Table of Content

A home equity loan is a type of loan in which the borrowers use the equity of their home as collateral. The loan amount is determined by the value of the property, and the value of the property is determined by an appraiser from the lending institution. A piggyback mortgage can include any additional mortgage loan beyond a borrower’s first mortgage loan that is secured with the same collateral. With a home equity loan, the borrower receives the loan proceeds all at once, while a HELOC allows a borrower to tap into the line as needed. Because the amount borrowed can change , the borrower’s minimum payments can also change, depending on the credit line’s usage. It allows the borrower to take out money against the credit line up to a preset limit, make payments, and then take out money again.

Fees are also required anytime you refinance your mortgage, so make sure you sit down and calculate your overall savings if you go this route. If you need to access a line of credit to make some purchases and you don’t expect to take more than a year to pay off your debt, you should consider a credit card with an introductory interest rate offer. Many of the top options let you earn rewards on your spending while enjoying zero interest on purchases or zero interest on balance transfers for 15 months or even longer. You will also likely need to pay for an appraisal to prove your home has enough value to support the loan, and you may also face document preparation fees, recording fees or broker fees as well. So it’s important to ask about fees up front and look for lenders who offer home equity loans with very limited “extra” fees and closing costs.

Balance transfer credit card

You’ll only pay interest on the cash you’ve borrowed, but, usually, at a variable rate. That means your monthly payment is subject to change as rates rise. These mortgages are tailor-made for homeowners age 62 or older, particularly those who have paid off their homes. Although you have a few options for receiving the money, one common approach is to have your lender send you a check each month, representating a small portion of the equity in your home. That gradually depletes your equity, and you'll be charged interest on what you're borrowing during the term of the mortgage.

If you have a 1st mortgage, you would need to combine that balance and the balance of the requested Home Equity Loan. If your home is worth $400,000, the maximum you could borrower would be $320,000. If your 1st mortgage balance is $280,000 you could request up to $40,000 for your Home Equity loan. If you’re considering a home equity loan, make sure to shop around and compare lenders, their rates and the fees they charge.

Bottom line: Are home equity loans a good idea?

Laura has also written for NextAdvisor, MoneyGeek, Personal Finance Insider, and The Financial Diet. Will look at your credit score and payment history to determine the loan interest rate. Her expertise includes mortgages, credit card rewards, and personal finance.

When it comes to a rental property, however, lenders typically require higher levels of equity for approval because it's a riskier loan for them. If a borrower falls behind on payments, the lender can seize the home, or collateral, in a process known as foreclosure. The lender then sells the home, often at an auction, to recoup its money. The original lender must be paid off in full before subsequent lenders receive any proceeds from a foreclosure sale. Home equity loans give the borrower a lump sum up front, and in return, they must make fixed payments over the life of the loan.

How To Get a Home Equity Loan

A home equity line of credit is similar to a credit card, acting as a revolving line of credit based on your home's equity. HELOC funds can be used when you need them, paid back, and used again. Often there is a 10-year draw period, where you can access your credit as needed, with interest-only payments. After the draw period, you enter the repayment period, where you must repay all the money you borrowed, plus interest. A cash-out refinance refers to using your equity to get a new mortgage that's larger than the amount owed on your existing mortgage. Then, you pay off the existing mortgage and use the remaining money as needed.

You’ll pay interest every month only on the amount you draw with options for interest-only payments. Most of the time HELOCs come with a variable or adjustable interest rate, which is good when rates are low but can be impossible to keep up with if they rise too quickly. A HELOC is a revolving line of credit, much like a credit card, that you can draw on as needed, pay back, and then draw on again, for a term determined by the lender.

You'll only pay interest on the amount you actually use from your pool of available money. Beware of red flags, like lenders who change the terms of the loan at the last minute or approve payments that you can’t afford. Suppose your home is valued at $300,000, and your mortgage balance is $225,000.

How much you can borrow depends on how much home equity you have, your credit score and other factors. A home equity loan calculator can help you estimate how much you might be able to borrow. Every lender operates at its own speed, but since the process to underwrite a home equity loan is similar to a standard mortgage, you can expect it to take about the same amount of time.

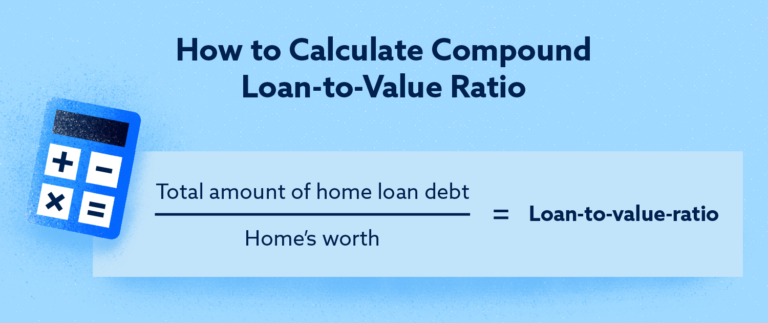

Millions of people have used our financial advice through 22 books published by Ramsey Press, as well as two syndicated radio shows and 10 podcasts, which have over 17 million weekly listeners. Most lenders want you to have a loan-to-value ratio that’s 80% or less. If you meet that criteria, they’ll approve you for a loan amount—usually up to 85% of your home equity. They also look at something called your loan-to-value ratio, which compares how much you owe on the house to how much equity you have. Even if you repaid part of the loan, the bank can’t just saw off the master bedroom so you can keep the part of the house you own.

Whatever the period, borrowers will have stable, predictable monthly payments to make for the life of the equity loan. It can be tempting to access all the cash that a home equity loan can provide, but it’s important not to treat your house as an ATM. Other times, home equity loans are used to consolidate other debts or to refinance a mortgage. Some people even use their home equity to make a down payment on another house.

The Federal Reserve has increased interest rates multiple times so far in 2022. Home equity loans still carried risks, but were relatively cheap with low payments. As interest rates rise, borrowing against your home’s equity means larger payments that may be harder to accommodate if your income decreases. The average annual interest rate for a home equity loan is around 6%.

No comments:

Post a Comment